-

Consumer Complaints Classification using Machine Learning and Deep Learning.

The dataset comprises of Consumer Complaints on Financial products and we’ll see how to classify consumer complaints text into these categories: Debt collection, Consumer Loan, Mortgage, Credit card, Credit reporting, Student loan, Bank account or service, Payday loan, Money transfers, Other financial service, Prepaid card.

The classification task would help banking/financial institution to quickly identify and provide customized solutions to each customer based on complaints received department wise. The dataset is available in link:- https://www.kaggle.com/cfpb/us-consumer-finance-complaints

We have performed initial analysis using text data with plots and word cloud for each department and performed various text pre-processing steps including Text Standardization,Removing Stopwords,Lemmatization,Spelling correction etc.Utilized Machine learning and Deep Learning methods to classify text data into 11 categories.

import numpy as np

import pandas as pd

from sklearn.feature_extraction.text import TfidfVectorizer

import sklearn.feature_extraction.text as text

from sklearn import model_selection, preprocessing, linear_model, naive_bayes, metrics, svm

from sklearn.naive_bayes import MultinomialNB

from sklearn.linear_model import LogisticRegression

from sklearn.ensemble import RandomForestClassifier

from sklearn.svm import LinearSVC

from sklearn.model_selection import cross_val_score

from sklearn.model_selection import train_test_split

from textblob import TextBlob

from nltk.stem import PorterStemmer,SnowballStemmer

from textblob import Word

from sklearn.feature_extraction.text import CountVectorizer,TfidfVectorizer

from nltk.corpus import stopwords

from nltk.tokenize import sent_tokenize, word_tokenize

from nltk.tokenize.toktok import ToktokTokenizer

from io import StringIO

import os

import string

import gensim

from gensim.models import Word2Vec

import itertools

import scipy

from scipy import spatial

import seaborn as sns

import matplotlib.pyplot as plt

import re

import nltk

tokenizer = ToktokTokenizer()

stopword_list = nltk.corpus.stopwords.words('english')

import warnings

warnings.filterwarnings("ignore")

nltk.download('stopwords')

[nltk_data] Downloading package stopwords to /home/hadoop/nltk_data...

[nltk_data] Package stopwords is already up-to-date!

True

nltk.download('wordnet')

[nltk_data] Downloading package wordnet to /home/hadoop/nltk_data...

[nltk_data] Package wordnet is already up-to-date!

True

df = pd.read_csv("consumer_complaints.csv")

df.head()

| date_received | product | sub_product | issue | sub_issue | consumer_complaint_narrative | company_public_response | company | state | zipcode | tags | consumer_consent_provided | submitted_via | date_sent_to_company | company_response_to_consumer | timely_response | consumer_disputed? | complaint_id | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 08/30/2013 | Mortgage | Other mortgage | Loan modification,collection,foreclosure | NaN | NaN | NaN | U.S. Bancorp | CA | 95993 | NaN | NaN | Referral | 09/03/2013 | Closed with explanation | Yes | Yes | 511074 |

| 1 | 08/30/2013 | Mortgage | Other mortgage | Loan servicing, payments, escrow account | NaN | NaN | NaN | Wells Fargo & Company | CA | 91104 | NaN | NaN | Referral | 09/03/2013 | Closed with explanation | Yes | Yes | 511080 |

| 2 | 08/30/2013 | Credit reporting | NaN | Incorrect information on credit report | Account status | NaN | NaN | Wells Fargo & Company | NY | 11764 | NaN | NaN | Postal mail | 09/18/2013 | Closed with explanation | Yes | No | 510473 |

| 3 | 08/30/2013 | Student loan | Non-federal student loan | Repaying your loan | Repaying your loan | NaN | NaN | Navient Solutions, Inc. | MD | 21402 | NaN | NaN | 08/30/2013 | Closed with explanation | Yes | Yes | 510326 | |

| 4 | 08/30/2013 | Debt collection | Credit card | False statements or representation | Attempted to collect wrong amount | NaN | NaN | Resurgent Capital Services L.P. | GA | 30106 | NaN | NaN | Web | 08/30/2013 | Closed with explanation | Yes | Yes | 511067 |

df.dtypes

date_received object

product object

sub_product object

issue object

sub_issue object

consumer_complaint_narrative object

company_public_response object

company object

state object

zipcode object

tags object

consumer_consent_provided object

submitted_via object

date_sent_to_company object

company_response_to_consumer object

timely_response object

consumer_disputed? object

complaint_id int64

dtype: object

df.describe(include='all')

| date_received | product | sub_product | issue | sub_issue | consumer_complaint_narrative | company_public_response | company | state | zipcode | tags | consumer_consent_provided | submitted_via | date_sent_to_company | company_response_to_consumer | timely_response | consumer_disputed? | complaint_id | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 555957 | 555957 | 397635 | 555957 | 212622 | 66806 | 85124 | 555957 | 551070 | 551452 | 77959 | 123458 | 555957 | 555957 | 555957 | 555957 | 555957 | 5.559570e+05 |

| unique | 1608 | 11 | 46 | 95 | 68 | 65646 | 10 | 3605 | 62 | 27052 | 3 | 4 | 6 | 1557 | 8 | 2 | 2 | NaN |

| top | 08/27/2015 | Mortgage | Other mortgage | Loan modification,collection,foreclosure | Account status | This company continues to report on my credit ... | Company chooses not to provide a public response | Bank of America | CA | 300XX | Older American | Consent provided | Web | 11/13/2015 | Closed with explanation | Yes | No | NaN |

| freq | 963 | 186475 | 74319 | 97191 | 26798 | 37 | 52478 | 55998 | 81700 | 1205 | 45257 | 66807 | 361338 | 1108 | 404293 | 541909 | 443823 | NaN |

| mean | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 9.600510e+05 |

| std | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 5.504296e+05 |

| min | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 1.000000e+00 |

| 25% | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 4.863230e+05 |

| 50% | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 9.737830e+05 |

| 75% | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 1.441702e+06 |

| max | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 1.895894e+06 |

df.isnull().sum()/df.shape[0]*100

date_received 0.000000

product 0.000000

sub_product 28.477382

issue 0.000000

sub_issue 61.755675

consumer_complaint_narrative 87.983603

company_public_response 84.688744

company 0.000000

state 0.879025

zipcode 0.810314

tags 85.977513

consumer_consent_provided 77.793606

submitted_via 0.000000

date_sent_to_company 0.000000

company_response_to_consumer 0.000000

timely_response 0.000000

consumer_disputed? 0.000000

complaint_id 0.000000

dtype: float64

df1 = df[['complaint_id','date_received','product','issue','company','state','submitted_via','company_response_to_consumer','timely_response','consumer_disputed?','consumer_complaint_narrative']]

df1 = df1[pd.notnull(df1['consumer_complaint_narrative'])]

EDA

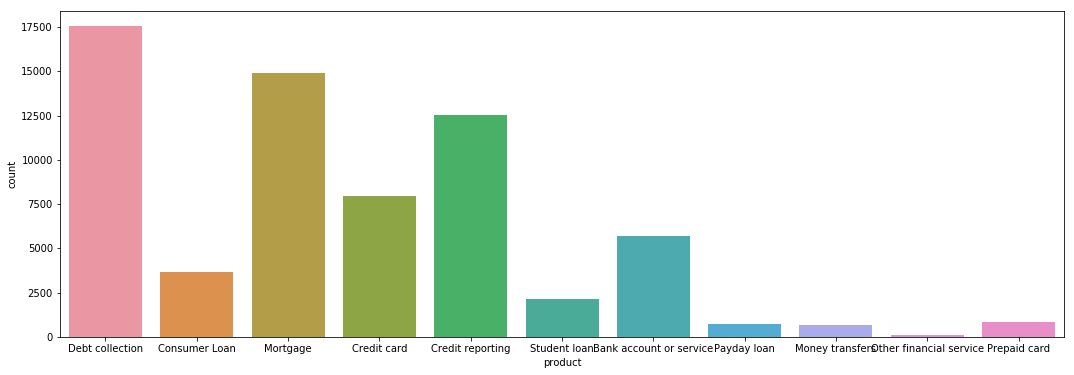

We’ll check the disribution of complaints by product category to understand which product received maximum complaints and other products which rarely receive complaints.

fig,ax = plt.subplots(figsize=(18,6))

sns.countplot(x='product',data=df1)

<matplotlib.axes._subplots.AxesSubplot at 0x7f7cf81fd0b8>

From this plot we can see Debt Collection and Mortgage received maximum number of complaints

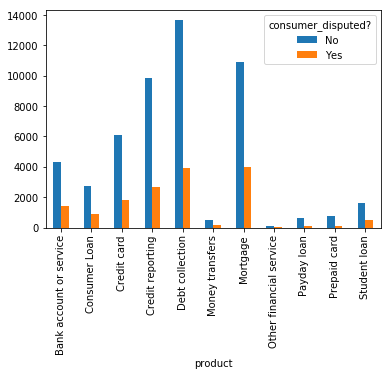

We’ll now analyze the contingency table in form of plot to understand which product has more customer disputes on their complaints after resolving the issues

pd.crosstab(df1['product'],df1['consumer_disputed?']).plot(kind='bar')

<matplotlib.axes._subplots.AxesSubplot at 0x7f7cf81a2b00>

Not much of difference in proportion of disputes raised by complaint for each product category.

Checking various plots to identify patterns within data

df1['date_received'] = pd.to_datetime(df1['date_received'])

df1.date_received.min(),df1.date_received.max()

(Timestamp('2015-03-19 00:00:00'), Timestamp('2016-04-20 00:00:00'))

df1['month'] = df1['date_received'].dt.month

sns.countplot(x='month',data=df1)

<matplotlib.axes._subplots.AxesSubplot at 0x7f7e1484dbe0>

sns.countplot(x='timely_response',data=df1)

<matplotlib.axes._subplots.AxesSubplot at 0x7f7e156f71d0>

Text Data Preprocessing

Converting Text data to Lowercase

df1['consumer_complaint_narrative'] =df1['consumer_complaint_narrative'].apply(lambda x: ' '.join([i.lower() for i in x.split()]))

df1['consumer_complaint_narrative'].sample(2)

519427 i underwent an xxxx, prior to xxxx. this was p...

324017 i got a loan through the money source in xxxx ...

Name: consumer_complaint_narrative, dtype: object

Removing Punctuations

df1['consumer_complaint_narrative'] =df1['consumer_complaint_narrative'].str.replace(r'[^\w\s]',"")

df1['consumer_complaint_narrative'].sample(2)

239441 every day im at work security financial from x...

512626 while on vacation my account became overdrawn ...

Name: consumer_complaint_narrative, dtype: object

Text standardization

#Below, we used three normalizazion dictionaries from these links :

#http://www.hlt.utdallas.edu/~yangl/data/Text_Norm_Data_Release_Fei_Liu/

#http://people.eng.unimelb.edu.au/tbaldwin/etc/emnlp2012-lexnorm.tgz

#http://luululu.com/tweet/typo-corpus-r1.txt

dico = {}

dico1 = open('doc1.txt', 'rb')

for word in dico1:

word = word.decode('utf8')

word = word.split()

dico[word[1]] = word[3]

dico1.close()

dico2 = open('doc2.txt', 'rb')

for word in dico2:

word = word.decode('utf8')

word = word.split()

dico[word[0]] = word[1]

dico2.close()

dico3 = open('doc3.txt', 'rb')

for word in dico3:

word = word.decode('utf8')

word = word.split()

dico[word[0]] = word[1]

dico3.close()

def txt_std(words):

list_words = words.split()

for i in range(len(list_words)):

if list_words[i] in dico.keys():

list_words[i] = dico[list_words[i]]

return ' '.join(list_words)

df1['consumer_complaint_narrative'] = df1['consumer_complaint_narrative'].apply(txt_std)

df1.consumer_complaint_narrative.head(1)

190126 xxxx has claimed i owe them 2700 for xxxx year...

Name: consumer_complaint_narrative, dtype: object

df1['consumer_complaint_narrative'] = df1['consumer_complaint_narrative'].str.replace(r"xx+\s","")

df1['consumer_complaint_narrative'].head(1)

190126 has claimed i owe them 2700 for years despite ...

Name: consumer_complaint_narrative, dtype: object

Removing Stopwords

from nltk.corpus import stopwords

stop = stopwords.words('english')

df1['consumer_complaint_narrative'] =df1['consumer_complaint_narrative'].apply(lambda x: ' '.join([i for i in x.split() if i not in stop]))

df1['consumer_complaint_narrative'].head(1)

190126 claimed owe 2700 years despite proof payment s...

Name: consumer_complaint_narrative, dtype: object

Correcting Spelling

##ensure text is standardized before applying this step

from textblob import TextBlob

df1['consumer_complaint_narrative'] =df1['consumer_complaint_narrative'].apply(lambda x: str(TextBlob(x).correct()))

Lemmatizing

from textblob import Word

df1['consumer_complaint_narrative'] =df1['consumer_complaint_narrative'].apply(lambda x:' '.join([Word(i).lemmatize() for i in x.split()]))

df1.consumer_complaint_narrative.head(1)

190126 claimed owe 2700 year despite proof payment se...

Name: consumer_complaint_narrative, dtype: object

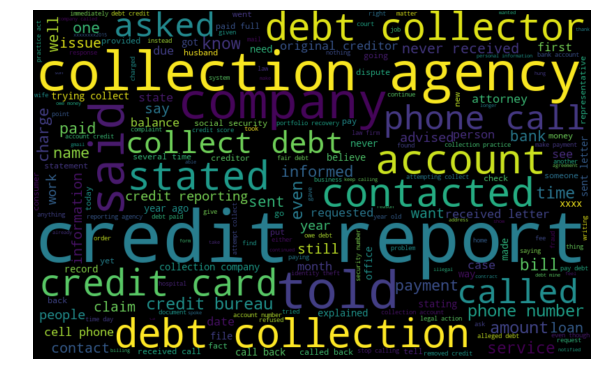

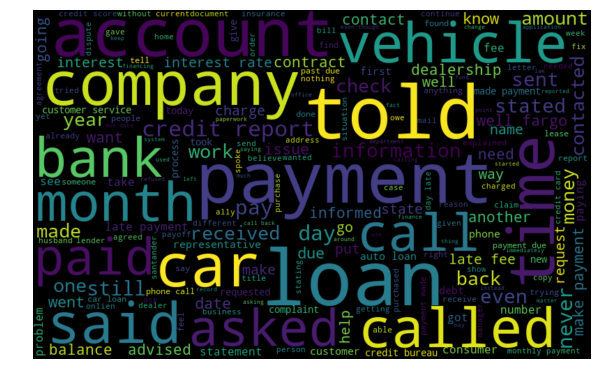

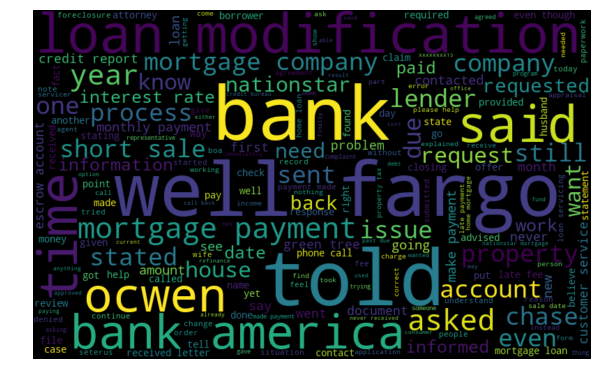

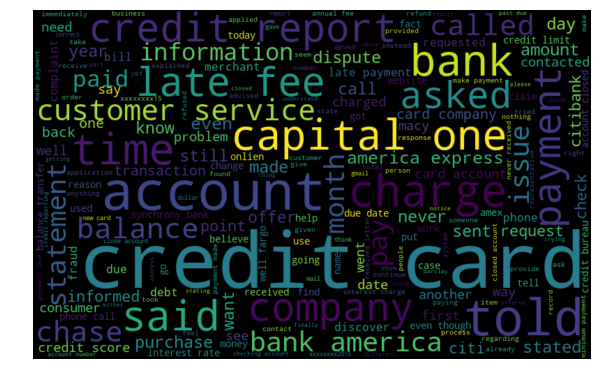

Word Cloud for all Product categories

for product_name in df1['product'].unique():

print(product_name)

all_words = ' '.join([text for text in df1.loc[df1['product'].str.contains(product_name),'consumer_complaint_narrative']])

from wordcloud import WordCloud

wordcloud = WordCloud(width=800, height=500, random_state=21, max_font_size=110).generate(all_words)

plt.figure(figsize=(10, 7))

plt.imshow(wordcloud, interpolation="bilinear")

plt.axis('off')

plt.show()

Debt collection

Consumer Loan

Mortgage

Credit card

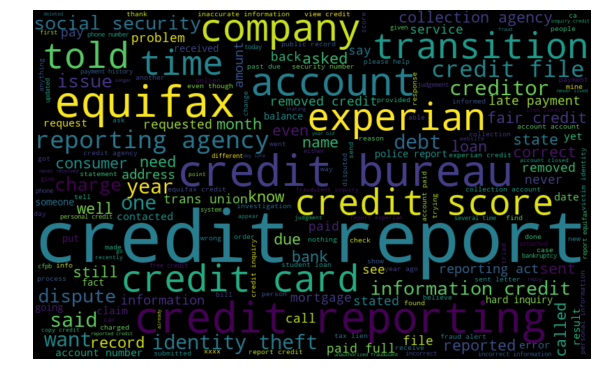

Credit reporting

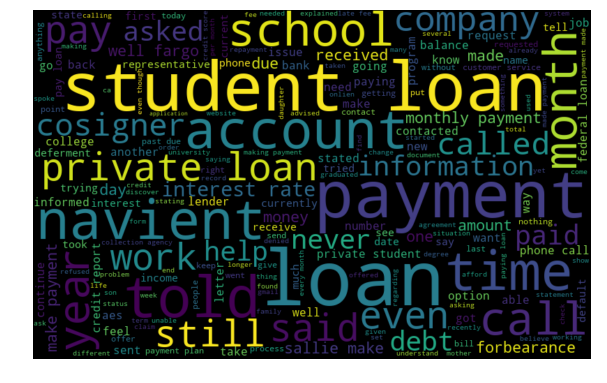

Student loan

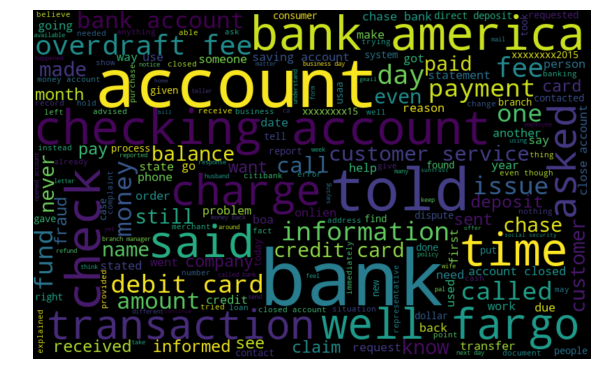

Bank account or service

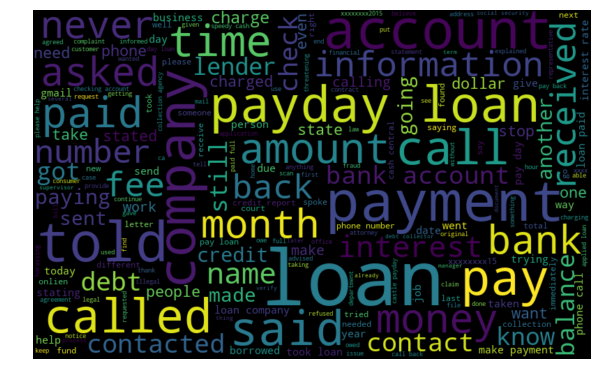

Payday loan

Money transfers

Other financial service

Prepaid card

Train/Test split

train_x, valid_x, train_y, valid_y = train_test_split(df1['consumer_complaint_narrative'], df1['product'],stratify=df1['product'],

test_size=0.25)

Feature engineering of consumer complaint with TF-IDF

##label encoding target variable

enc = preprocessing.LabelEncoder()

train_y = enc.fit_transform(train_y)

valid_y = enc.fit_transform(valid_y)

##tf-idf verctor representation

tfidf_vect = TfidfVectorizer(analyzer='word', token_pattern=r'\w{1,}', max_features=5000)

tfidf_vect.fit(df1['consumer_complaint_narrative'])

xtrain_tfidf = tfidf_vect.transform(train_x)

xvalid_tfidf = tfidf_vect.transform(valid_x)

from sklearn.model_selection import GridSearchCV

clf = LogisticRegression()

lr_params = {'C':[int(x) for x in np.linspace(1,10,10)]}

grid_lr = GridSearchCV(estimator=clf,param_grid=lr_params,cv=5,n_jobs=-1)

grid_lr.fit(xtrain_tfidf,train_y)

GridSearchCV(cv=5, error_score='raise-deprecating',

estimator=LogisticRegression(C=1.0, class_weight=None, dual=False, fit_intercept=True,

intercept_scaling=1, max_iter=100, multi_class='warn',

n_jobs=None, penalty='l2', random_state=None, solver='warn',

tol=0.0001, verbose=0, warm_start=False),

fit_params=None, iid='warn', n_jobs=-1,

param_grid={'C': [1, 2, 3, 4, 5, 6, 7, 8, 9, 10]},

pre_dispatch='2*n_jobs', refit=True, return_train_score='warn',

scoring=None, verbose=0)

print(grid_lr.best_params_)

print(grid_lr.best_score_)

{'C': 5}

0.8462398211719623

final_lr = LogisticRegression(C=5)

final_lr.fit(xtrain_tfidf,train_y)

LogisticRegression(C=5, class_weight=None, dual=False, fit_intercept=True,

intercept_scaling=1, max_iter=100, multi_class='warn',

n_jobs=None, penalty='l2', random_state=None, solver='warn',

tol=0.0001, verbose=0, warm_start=False)

final_lr_predict = final_lr.predict(xvalid_tfidf)

lr_accuracy = metrics.accuracy_score(final_lr_predict, valid_y)

print ("Logistic Regression > Accuracy: ", lr_accuracy)

Logistic Regression > Accuracy: 0.8506765656807568

from sklearn.metrics import classification_report

print(classification_report(valid_y, final_lr_predict,target_names=df1['product'].unique()))

precision recall f1-score support

Debt collection 0.83 0.79 0.81 1428

Consumer Loan 0.77 0.62 0.69 920

Mortgage 0.80 0.83 0.81 1982

Credit card 0.86 0.85 0.86 3132

Credit reporting 0.83 0.89 0.85 4388

Student loan 0.77 0.64 0.70 166

Bank account or service 0.93 0.96 0.94 3730

Payday loan 1.00 0.04 0.07 27

Money transfers 0.68 0.36 0.47 182

Other financial service 0.80 0.70 0.74 215

Prepaid card 0.87 0.77 0.82 532

micro avg 0.85 0.85 0.85 16702

macro avg 0.83 0.68 0.71 16702

weighted avg 0.85 0.85 0.85 16702

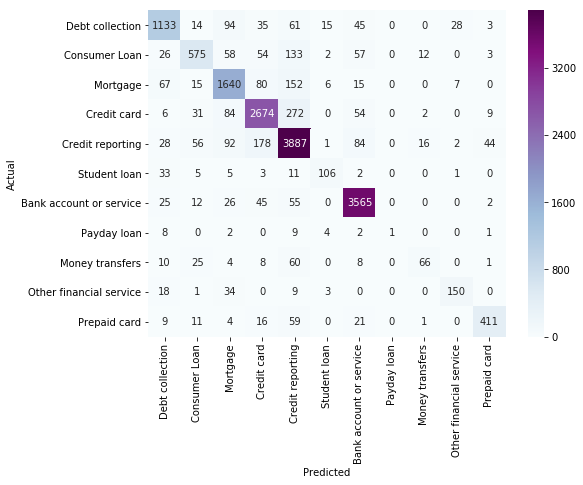

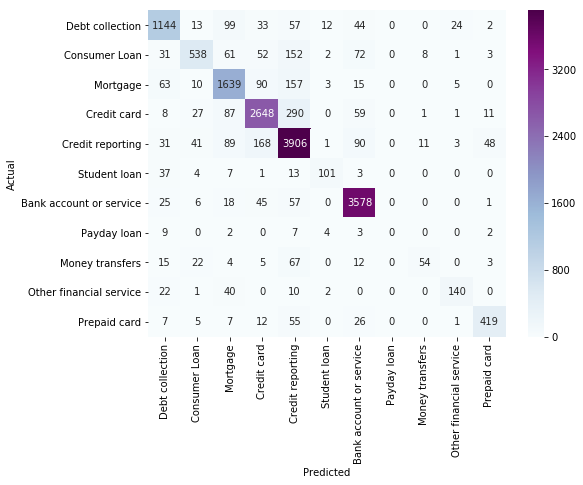

from sklearn.metrics import confusion_matrix

conf_mat = confusion_matrix(valid_y, final_lr_predict)

fig, ax = plt.subplots(figsize=(8,6))

sns.heatmap(conf_mat, annot=True, fmt="d", cmap="BuPu",xticklabels=df1['product'].unique(),yticklabels=df1['product'].unique())

plt.ylabel('Actual')

plt.xlabel('Predicted')

plt.show()

We have acheived an accuracy of around 85% with a Logistic Regression model and the classification metrics are good for all departments except Payday loan - this might be due to less training instances of this product category and also on looking at the confusion matrix it is mostly being predicted as Credit reporting or debt collection which gives us an indication that this product is similar to one another or maybe linked with other.

We might further improve the performance using Random Forest, SVM, GBM, Neural Networks and utilize hyperparameter tuning.

SVM

from sklearn.svm import LinearSVC

svc_model = LinearSVC()

svc_params = {'C':[0.01,0.1, 1, 10, 100, 1000]}

grid_svc = GridSearchCV(estimator=svc_model,param_grid=svc_params,cv=5,n_jobs=-1)

grid_svc.fit(xtrain_tfidf,train_y)

GridSearchCV(cv=5, error_score='raise-deprecating',

estimator=LinearSVC(C=1.0, class_weight=None, dual=True, fit_intercept=True,

intercept_scaling=1, loss='squared_hinge', max_iter=1000,

multi_class='ovr', penalty='l2', random_state=None, tol=0.0001,

verbose=0),

fit_params=None, iid='warn', n_jobs=-1,

param_grid={'C': [0.01, 0.1, 1, 10, 100, 1000]},

pre_dispatch='2*n_jobs', refit=True, return_train_score='warn',

scoring=None, verbose=0)

print(grid_svc.best_params_)

print(grid_svc.best_score_)

{'C': 0.1}

0.8435055085422322

final_svc = LinearSVC(C=0.1)

final_svc.fit(xtrain_tfidf,train_y)

LinearSVC(C=0.1, class_weight=None, dual=True, fit_intercept=True,

intercept_scaling=1, loss='squared_hinge', max_iter=1000,

multi_class='ovr', penalty='l2', random_state=None, tol=0.0001,

verbose=0)

final_svc_predict = final_svc.predict(xvalid_tfidf)

svc_accuracy = metrics.accuracy_score(final_svc_predict, valid_y)

print ("SVC > Accuracy: ", svc_accuracy)

SVC > Accuracy: 0.8482217698479224

print(classification_report(valid_y, final_svc_predict,target_names=df1['product'].unique()))

precision recall f1-score support

Debt collection 0.82 0.80 0.81 1428

Consumer Loan 0.81 0.58 0.68 920

Mortgage 0.80 0.83 0.81 1982

Credit card 0.87 0.85 0.86 3132

Credit reporting 0.82 0.89 0.85 4388

Student loan 0.81 0.61 0.69 166

Bank account or service 0.92 0.96 0.94 3730

Payday loan 0.00 0.00 0.00 27

Money transfers 0.73 0.30 0.42 182

Other financial service 0.80 0.65 0.72 215

Prepaid card 0.86 0.79 0.82 532

micro avg 0.85 0.85 0.85 16702

macro avg 0.75 0.66 0.69 16702

weighted avg 0.85 0.85 0.84 16702

conf_mat = confusion_matrix(valid_y, final_svc_predict)

fig, ax = plt.subplots(figsize=(8,6))

sns.heatmap(conf_mat, annot=True, fmt="d", cmap="BuPu",xticklabels=df1['product'].unique(),yticklabels=df1['product'].unique())

plt.ylabel('Actual')

plt.xlabel('Predicted')

plt.show()

XGBOOST

from xgboost import XGBClassifier

xgb_model = XGBClassifier(max_depth=50, n_estimators=80, learning_rate=0.1, colsample_bytree=.7, gamma=0, reg_alpha=4, eta=0.3, silent=1, subsample=0.8)

xgb_model.fit(xtrain_tfidf_final, train_y)

XGBClassifier(base_score=0.5, booster='gbtree', colsample_bylevel=1,

colsample_bytree=0.7, eta=0.3, gamma=0, learning_rate=0.1,

max_delta_step=0, max_depth=50, min_child_weight=1, missing=None,

n_estimators=80, n_jobs=1, nthread=None, objective='multi:softprob',

random_state=0, reg_alpha=4, reg_lambda=1, scale_pos_weight=1,

seed=None, silent=1, subsample=0.8)

xgb_predict = xgb_model.predict(xvalid_tfidf_final)

xgb_accuracy = metrics.accuracy_score(xgb_predict, valid_y)

print ("XGBoost > Accuracy: ", xgb_accuracy)

XGBoost > Accuracy: 0.8533708537899652

from sklearn.metrics import classification_report

print(classification_report(valid_y, xgb_predict,target_names=df1['product'].unique()))

precision recall f1-score support

Debt collection 0.83 0.81 0.82 1432

Consumer Loan 0.77 0.60 0.67 936

Mortgage 0.81 0.82 0.82 1987

Credit card 0.86 0.87 0.87 3138

Credit reporting 0.83 0.89 0.86 4384

Student loan 0.89 0.59 0.71 173

Bank account or service 0.92 0.95 0.94 3704

Payday loan 1.00 0.05 0.10 19

Money transfers 0.60 0.37 0.45 178

Other financial service 0.82 0.73 0.77 220

Prepaid card 0.88 0.85 0.87 531

micro avg 0.85 0.85 0.85 16702

macro avg 0.84 0.68 0.72 16702

weighted avg 0.85 0.85 0.85 16702

from sklearn.metrics import confusion_matrix

conf_mat = confusion_matrix(valid_y, xgb_predict)

fig, ax = plt.subplots(figsize=(8,6))

sns.heatmap(conf_mat, annot=True, fmt="d", cmap="BuPu",xticklabels=df1['product'].unique(),yticklabels=df1['product'].unique())

plt.ylabel('Actual')

plt.xlabel('Predicted')

plt.show()

Deep Learning models

from keras.preprocessing.text import Tokenizer

from keras.preprocessing.sequence import pad_sequences

from keras.utils import to_categorical

from keras.layers import Dense, Input, LSTM, Embedding, Dropout, Activation

from keras.layers import Bidirectional, GlobalMaxPool1D, Conv1D, SimpleRNN

from keras.models import Model

from keras.models import Sequential

from keras import initializers, regularizers, constraints, optimizers, layers

from keras.layers import Dense, Input, Flatten, Dropout, BatchNormalization

from keras.layers import Conv1D, MaxPooling1D, Embedding

from keras.models import Sequential

Using TensorFlow backend.

#total_complaints = np.append(train_x.values,valid_x.values)

tokenizer = Tokenizer(num_words=25000)

tokenizer.fit_on_texts(train_x.values)#total_complaints

train_sequences = tokenizer.texts_to_sequences(train_x.values)

test_sequences = tokenizer.texts_to_sequences(valid_x.values)

word_index = tokenizer.word_index# dictionary containing words and their index

print('Found %s unique tokens.' % len(word_index))

Found 51128 unique tokens.

MAX_SEQUENCE_LENGTH = max([len(c.split()) for c in total_complaints])

MAX_SEQUENCE_LENGTH

394

train_data = pad_sequences(train_sequences, maxlen=max_length,padding='post')

test_data = pad_sequences(test_sequences, maxlen=max_length,padding='post')

print(train_data.shape)

print(test_data.shape)

(50104, 394)

(16702, 394)

enc = preprocessing.LabelEncoder()

train_labels = enc.fit_transform(train_y)

test_labels = enc.fit_transform(valid_y)

print(enc.classes_)

print(np.unique(train_labels, return_counts=True))

print(np.unique(test_labels, return_counts=True))

['Bank account or service' 'Consumer Loan' 'Credit card'

'Credit reporting' 'Debt collection' 'Money transfers' 'Mortgage'

'Other financial service' 'Payday loan' 'Prepaid card' 'Student loan']

(array([ 0, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10]), array([ 4283, 2758, 5947, 9394, 13164, 500, 11189, 83, 544,

646, 1596]))

(array([ 0, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10]), array([1428, 920, 1982, 3132, 4388, 166, 3730, 27, 182, 215, 532]))

labels_train = to_categorical(np.asarray(train_labels))

labels_test = to_categorical(np.asarray(test_labels))

print('Shape of data tensor:', train_data.shape)

print('Shape of label tensor:', labels_train.shape)

print('Shape of label tensor:', labels_test.shape)

Shape of data tensor: (50104, 394)

Shape of label tensor: (50104, 11)

Shape of label tensor: (16702, 11)

CNN w/ Pre-trained word embeddings(GloVe)

We’ll use pre-trained embeddings such as Glove which provides word based vector representation trained on a large corpus.

It is trained on a dataset of one billion tokens (words) with a vocabulary of 400 thousand words. The glove has embedding vector sizes, including 50, 100, 200 and 300 dimensions.

#wget http://nlp.stanford.edu/data/glove.6B.zip

GLOVE_DIR = '/mnt/data/temp/nlp/'

embeddings_index = {}

f = open(os.path.join(GLOVE_DIR, 'glove.6B.300d.txt'))

for line in f:

values = line.split()

word = values[0]

coefs = np.asarray(values[1:], dtype='float32')

embeddings_index[word] = coefs

f.close()

print('Found %s word vectors.' % len(embeddings_index))

Found 400000 word vectors.

Now lets create the embedding matrix using the word indexer created from tokenizer.

EMBEDDING_DIM = 300

embedding_matrix = np.zeros((len(word_index) + 1, EMBEDDING_DIM))

for word, i in word_index.items():

embedding_vector = embeddings_index.get(word)

if embedding_vector is not None:

# words not found in embedding index will be all-zeros.

embedding_matrix[i] = embedding_vector

Lets check the word embedded vector representation for token ‘loan’ in our embedding matrix

[(k,v) for k,v in word_index.items() if v==4]

[('loan', 4)]

embedding_matrix[4] ## word embedded vector representation for token 'loan'

array([ 0.13474999, 0.063568 , -0.37950999, -0.080729 , 0.34176001,

-0.0053481 , 0.80001003, -0.78824002, -0.47262999, -0.89402002,

0.086908 , -0.051773 , 0.57349998, -0.26681 , -0.0043554 ,

-0.68673003, 0.54759002, -0.47711 , 0.12997 , -0.50748003,

0.073666 , -0.56199998, 0.19243 , -0.022735 , 0.15757 ,

0.68008 , -0.48374999, 0.14399 , -0.69022 , 0.26741001,

-0.53082001, -0.29096001, 0.32907999, 0.12313 , -1.14779997,

-0.51828998, -0.018956 , 0.02077 , -0.0015803 , -0.053114 ,

-0.10982 , -0.83578998, -0.46337 , 0.85992002, 0.57225001,

-0.33202001, -0.23357999, 0.80937999, -0.43586999, 0.35385001,

0.0055405 , 0.068909 , 0.13897 , 0.16237999, 0.038382 ,

-0.16306999, -0.022701 , 0.14324 , -0.25878 , -0.47661999,

0.25588 , -0.23389 , -0.14936 , -0.51688999, 0.44329 ,

0.49015 , 0.25725001, -0.45041999, 0.66949999, -0.32949001,

0.34626999, 0.91883999, 0.29245001, 0.20112 , 0.19018 ,

0.17321999, -0.3028 , 0.34022999, 0.49851999, -0.66885 ,

0.046698 , -0.19625001, -0.18028 , -0.41620001, 0.25986001,

-0.078103 , -0.33655 , 0.2077 , -0.69224 , 0.13703001,

-0.078832 , 0.26159 , -0.81893998, -0.35289001, 0.93794 ,

-0.1078 , -0.0944 , -0.11647 , 0.16785 , -0.32293001,

0.26176 , -0.37233001, 0.20868 , 0.040312 , -0.10222 ,

0.03121 , -0.09023 , 0.10476 , -0.042395 , 0.43564999,

0.18483 , -0.37215999, -0.21328001, -0.38079 , 0.39579999,

-0.32354999, 0.36971 , 0.036001 , 0.27676001, -0.19016001,

0.45638999, -0.16368 , -0.28349 , 1.09430003, 0.42951 ,

0.31263 , -0.24164 , -0.65586001, 0.42745 , 0.062487 ,

0.13004 , 0.40292001, 0.36722001, 0.2735 , 0.41966999,

0.22131 , 0.11602 , 0.22048999, -0.70600998, -0.35673001,

0.30159 , 0.1577 , 0.50809997, -0.17802 , -0.1236 ,

0.039545 , -0.47681001, -0.27853999, 0.022819 , -0.34139001,

0.057525 , -0.19609 , -0.47088999, -0.094618 , 0.03156 ,

0.17686 , 0.1304 , -0.19153 , -1.01779997, 0.27147001,

-0.094474 , 0.19495 , -0.22766 , 0.48361999, -0.15542001,

-0.31952 , 0.18727 , -0.20431 , 0.17941 , 0.39689001,

-0.22562 , 0.22657 , -0.39245999, 0.13325 , 0.11315 ,

-0.0089568 , -0.39331999, -0.42818999, -0.050899 , 0.98714 ,

0.70963001, -0.73843002, 0.0015733 , -0.22325 , -0.032507 ,

0.068939 , -0.061416 , 0.27745 , 0.81079 , 0.068871 ,

-0.11854 , 1.23679996, -0.2137 , 0.14869 , -0.10408 ,

-0.28125 , 0.44893 , -0.020156 , -0.24044999, -0.26190999,

0.39906001, 0.083602 , -0.36026001, 0.099067 , 0.32196999,

-0.52192003, -0.20076001, 0.22297999, -0.55962998, -0.043737 ,

-0.11283 , -0.12897 , 0.087192 , -0.27746001, 0.36127999,

0.50796002, 0.0031916 , 0.42192 , -0.61040002, 0.31369001,

0.32049 , -0.29355001, -0.59398001, -0.24123 , 0.052429 ,

-0.21264 , -0.086706 , 0.21190999, 0.15614 , 0.20209999,

-0.52890998, 0.22271 , -0.034363 , -0.047417 , 0.57754999,

-0.13970999, -0.1857 , 0.30785999, 0.903 , 0.33508 ,

0.84836 , 0.14651 , 0.65511 , -0.13307001, -0.89139003,

0.45642 , -0.027791 , -0.70120001, -0.036094 , -0.048917 ,

-0.28738999, 0.37559 , 0.19429 , 0.26212001, 0.27517 ,

-0.20432 , -1.36479998, 0.41104999, 0.21875 , 0.023549 ,

-0.37918001, 0.90345001, -0.061026 , 0.39754999, -0.30871999,

0.066477 , 0.36392999, 0.30715999, -0.010557 , -0.068205 ,

0.43869999, -0.39995 , -0.67673999, 0.41769999, 1.01440001,

-0.043677 , -0.87041003, -0.43674999, 0.53908998, 0.13293 ,

-0.16768999, -0.033394 , 0.29978001, 0.24638 , 0.077386 ,

0.73455 , 0.20106 , -0.31229001, 0.44185999, -0.64885002,

-0.50042999, 0.40474001, -0.31336999, -0.93396997, 1.26020002,

0.38231999, 0.51256001, -0.27717999, -0.83829999, 0.19851001])

vocab_size = len(tokenizer.word_index)+1

Now we load this embedding matrix into an Embedding layer using Sequential API to form a Convolutional NeuralNet model.

Dropout is applied between the hidden layers to factor regularization and prevent overfitting of neural network.

model = Sequential()

model.add(Embedding(len(word_index) + 1,

EMBEDDING_DIM,

weights=[embedding_matrix],

input_length=MAX_SEQUENCE_LENGTH,

trainable=True))

model.add(Dropout(0.3))

model.add(Conv1D(128, 5, activation="relu"))

model.add(MaxPooling1D(5))

model.add(Dropout(0.3))

model.add(BatchNormalization())

model.add(Conv1D(128, 5, activation="relu"))

model.add(MaxPooling1D(5))

model.add(Dropout(0.3))

model.add(BatchNormalization())

model.add(Flatten())

model.add(Dense(128, activation="relu"))

model.add(Dense(11, activation="softmax"))

model.compile(loss='categorical_crossentropy',

optimizer="rmsprop",

metrics=['acc'])

history = model.fit(train_data, labels_train,

batch_size=64,

epochs=8,

validation_data=(test_data, labels_test))

Train on 50104 samples, validate on 16702 samples

Epoch 1/8

50104/50104 [==============================] - 44s 872us/step - loss: 0.9975 - acc: 0.6868 - val_loss: 0.6876 - val_acc: 0.7930

Epoch 2/8

50104/50104 [==============================] - 41s 816us/step - loss: 0.6593 - acc: 0.8016 - val_loss: 0.5794 - val_acc: 0.8284

Epoch 3/8

50104/50104 [==============================] - 42s 836us/step - loss: 0.5721 - acc: 0.8300 - val_loss: 0.5572 - val_acc: 0.8400

Epoch 4/8

50104/50104 [==============================] - 42s 832us/step - loss: 0.5236 - acc: 0.8423 - val_loss: 0.5348 - val_acc: 0.8419

Epoch 5/8

50104/50104 [==============================] - 41s 826us/step - loss: 0.4910 - acc: 0.8520 - val_loss: 0.5241 - val_acc: 0.8502

Epoch 6/8

50104/50104 [==============================] - 41s 810us/step - loss: 0.4615 - acc: 0.8612 - val_loss: 0.5449 - val_acc: 0.8505

Epoch 7/8

50104/50104 [==============================] - 41s 809us/step - loss: 0.4447 - acc: 0.8687 - val_loss: 0.5550 - val_acc: 0.8528

Epoch 8/8

50104/50104 [==============================] - 41s 811us/step - loss: 0.4213 - acc: 0.8735 - val_loss: 0.5559 - val_acc: 0.8568

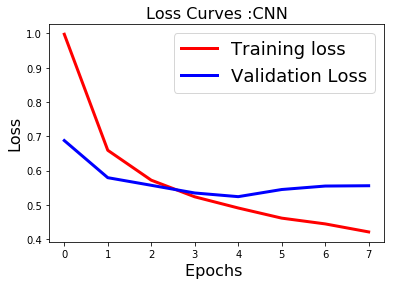

fig1 = plt.figure()

plt.plot(history.history['loss'],'r',linewidth=3.0)

plt.plot(history.history['val_loss'],'b',linewidth=3.0)

plt.legend(['Training loss', 'Validation Loss'],fontsize=18)

plt.xlabel('Epochs ',fontsize=16)

plt.ylabel('Loss',fontsize=16)

plt.title('Loss Curves :CNN',fontsize=16)

plt.show()

After 3 epochs the CNN tends to be overfitting the training data and therefore we need to implement early stopping to prevent such instances of overfitting and tune the number of epochs during training.

#predictions on test data

predicted=model.predict(test_data)

predicted

array([[8.07726883e-06, 6.62703314e-05, 1.78964832e-03, ...,

6.29637427e-08, 1.20558980e-07, 1.14476046e-04],

[2.95381608e-10, 1.03029949e-08, 1.18816992e-08, ...,

3.01563633e-19, 2.13277332e-30, 3.77692539e-12],

[5.53291329e-06, 1.50882616e-03, 4.29511711e-04, ...,

5.21915681e-05, 5.36095501e-10, 1.35198381e-04],

...,

[3.19875457e-04, 2.95074121e-03, 7.61984801e-03, ...,

5.84271547e-05, 3.93354838e-07, 1.12289046e-04],

[5.23970462e-03, 1.25093470e-06, 5.79587542e-08, ...,

3.22076106e-13, 1.34494688e-22, 5.08515097e-09],

[1.74894019e-08, 1.55232010e-05, 1.46042012e-05, ...,

8.76272254e-14, 4.28086869e-22, 6.98745950e-08]], dtype=float32)

#model evaluation

import sklearn

from sklearn.metrics import precision_recall_fscore_support as score

precision, recall, fscore, support = score(labels_test, predicted.round())

print('precision: \n{}'.format(precision))

print('recall: \n{}'.format(recall))

print('fscore: \n{}'.format(fscore))

print('support: \n{}'.format(support))

precision:

[0.86736334 0.76771654 0.85052632 0.90071648 0.86662138 0.58522727

0.93119625 0. 0.55696203 0.74770642 0.88888889]

recall:

[0.75560224 0.63586957 0.81533804 0.84291188 0.87215132 0.62048193

0.95790885 0. 0.24175824 0.75813953 0.82706767]

fscore:

[0.80763473 0.69560048 0.83256054 0.87085601 0.86937756 0.60233918

0.94436368 0. 0.33716475 0.75288684 0.85686465]

support:

[1428 920 1982 3132 4388 166 3730 27 182 215 532]

print(classification_report(labels_test, predicted.round(),target_names=df1['product'].unique()))

precision recall f1-score support

Debt collection 0.87 0.76 0.81 1428

Consumer Loan 0.77 0.64 0.70 920

Mortgage 0.85 0.82 0.83 1982

Credit card 0.90 0.84 0.87 3132

Credit reporting 0.87 0.87 0.87 4388

Student loan 0.59 0.62 0.60 166

Bank account or service 0.93 0.96 0.94 3730

Payday loan 0.00 0.00 0.00 27

Money transfers 0.56 0.24 0.34 182

Other financial service 0.75 0.76 0.75 215

Prepaid card 0.89 0.83 0.86 532

micro avg 0.88 0.84 0.86 16702

macro avg 0.72 0.67 0.69 16702

weighted avg 0.87 0.84 0.86 16702

samples avg 0.84 0.84 0.84 16702

Now, we’ll initialize our Embedding layer from scratch and learning its weights during training instead of using a pre-trained word embeddings and build a small 1D convnet to solve our classification problem.

#The Embedding layer requires the specification of the vocabulary size (vocab_size),

#the size of the real-valued vector space EMBEDDING_DIM = 100,

#and the maximum length of input documents max_length .

vocab_size = len(tokenizer.word_index)+1

EMBEDDING_DIM = 300

max_length = 394

model = Sequential()

model.add(Embedding(vocab_size,

300,

input_length=max_length

))

model.add(Dropout(0.3))

model.add(Conv1D(128, 5, activation="relu"))

model.add(MaxPooling1D(5))

model.add(Dropout(0.3))

model.add(BatchNormalization())

model.add(Conv1D(128, 5, activation="relu"))

model.add(MaxPooling1D(5))

model.add(Dropout(0.3))

model.add(BatchNormalization())

model.add(Flatten())

model.add(Dense(128, activation="relu"))

model.add(Dense(11, activation="softmax"))

model.compile(loss='categorical_crossentropy',

optimizer="rmsprop",

metrics=['acc'])

history = model.fit(train_data, labels_train,

batch_size=64,

epochs=8,

validation_data=(test_data, labels_test))

Train on 50104 samples, validate on 16702 samples

Epoch 1/8

50104/50104 [==============================] - 43s 848us/step - loss: 0.9356 - acc: 0.7071 - val_loss: 0.6082 - val_acc: 0.8227

Epoch 2/8

50104/50104 [==============================] - 40s 806us/step - loss: 0.5783 - acc: 0.8288 - val_loss: 0.6060 - val_acc: 0.8333

Epoch 3/8

50104/50104 [==============================] - 42s 836us/step - loss: 0.5033 - acc: 0.8511 - val_loss: 0.5611 - val_acc: 0.8443

Epoch 4/8

50104/50104 [==============================] - 40s 795us/step - loss: 0.4559 - acc: 0.8647 - val_loss: 0.5789 - val_acc: 0.8498

Epoch 5/8

50104/50104 [==============================] - 40s 798us/step - loss: 0.4272 - acc: 0.8749 - val_loss: 0.5795 - val_acc: 0.8498

Epoch 6/8

50104/50104 [==============================] - 40s 795us/step - loss: 0.3885 - acc: 0.8861 - val_loss: 0.5923 - val_acc: 0.8511

Epoch 7/8

50104/50104 [==============================] - 39s 786us/step - loss: 0.3639 - acc: 0.8929 - val_loss: 0.6127 - val_acc: 0.8492

Epoch 8/8

50104/50104 [==============================] - 40s 795us/step - loss: 0.3355 - acc: 0.9011 - val_loss: 0.7113 - val_acc: 0.8431

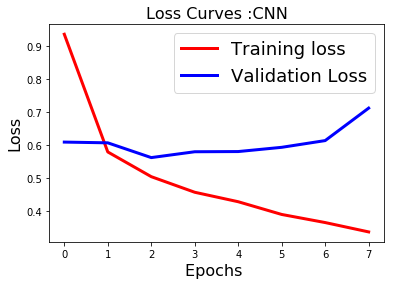

fig1 = plt.figure()

plt.plot(history.history['loss'],'r',linewidth=3.0)

plt.plot(history.history['val_loss'],'b',linewidth=3.0)

plt.legend(['Training loss', 'Validation Loss'],fontsize=18)

plt.xlabel('Epochs ',fontsize=16)

plt.ylabel('Loss',fontsize=16)

plt.title('Loss Curves :CNN',fontsize=16)

plt.show()

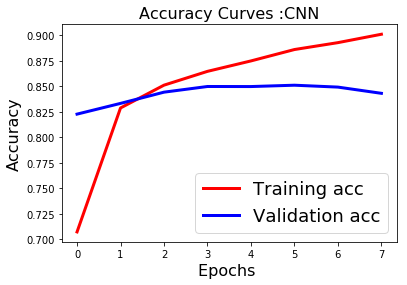

fig1 = plt.figure()

plt.plot(history.history['acc'],'r',linewidth=3.0)

plt.plot(history.history['val_acc'],'b',linewidth=3.0)

plt.legend(['Training acc', 'Validation acc'],fontsize=18)

plt.xlabel('Epochs ',fontsize=16)

plt.ylabel('Accuracy',fontsize=16)

plt.title('Accuracy Curves :CNN',fontsize=16)

plt.show()

#predictions on test data

predicted=model.predict(test_data)

predicted

array([[8.0981451e-08, 1.0855978e-04, 2.4081068e-04, ..., 1.2183374e-08,

4.2278413e-14, 1.3356260e-03],

[4.4842030e-15, 4.8303903e-17, 3.0950001e-14, ..., 1.1857974e-27,

4.1175130e-29, 2.4889569e-18],

[8.0113517e-07, 8.7012697e-05, 2.1043130e-04, ..., 1.1248574e-05,

6.5152328e-11, 3.9855800e-06],

...,

[1.1208030e-05, 1.1443447e-04, 8.2766742e-04, ..., 7.2765088e-06,

4.9168783e-08, 2.9500878e-05],

[1.1967868e-06, 7.0446168e-07, 2.0910631e-09, ..., 1.2298947e-12,

4.2028167e-27, 5.5382466e-06],

[1.0300022e-10, 7.4779948e-12, 9.7130914e-10, ..., 5.6786068e-19,

2.3970355e-20, 9.0075374e-14]], dtype=float32)

#model evaluation

import sklearn

from sklearn.metrics import precision_recall_fscore_support as score

precision, recall, fscore, support = score(labels_test, predicted.round())

print('precision: {}'.format(precision))

print('recall: {}'.format(recall))

print('fscore: {}'.format(fscore))

print('support: {}'.format(support))

print("############################")

print(sklearn.metrics.classification_report(labels_test, predicted.round()))

precision: [0.86960203 0.83412322 0.85229759 0.90954594 0.77928102 0.74038462

0.93012871 0. 0.58653846 0.76732673 0.89770355]

recall: [0.71918768 0.57391304 0.78607467 0.81226054 0.91886964 0.46385542

0.94932976 0. 0.33516484 0.72093023 0.80827068]

fscore: [0.78727482 0.67997424 0.81784777 0.85815483 0.84333821 0.57037037

0.93963115 0. 0.42657343 0.74340528 0.85064293]

support: [1428 920 1982 3132 4388 166 3730 27 182 215 532]

############################

precision recall f1-score support

0 0.87 0.72 0.79 1428

1 0.83 0.57 0.68 920

2 0.85 0.79 0.82 1982

3 0.91 0.81 0.86 3132

4 0.78 0.92 0.84 4388

5 0.74 0.46 0.57 166

6 0.93 0.95 0.94 3730

7 0.00 0.00 0.00 27

8 0.59 0.34 0.43 182

9 0.77 0.72 0.74 215

10 0.90 0.81 0.85 532

micro avg 0.86 0.84 0.85 16702

macro avg 0.74 0.64 0.68 16702

weighted avg 0.86 0.84 0.84 16702

samples avg 0.84 0.84 0.84 16702

RNN

#Bidirectional LSTM

model = Sequential()

model.add(Embedding(len(word_index) + 1,

EMBEDDING_DIM,

weights=[embedding_matrix],

input_length=MAX_SEQUENCE_LENGTH,

trainable=True))

model.add(Bidirectional(LSTM(100, dropout_U = 0.2, dropout_W = 0.2)))

model.add(Dense(11,activation='softmax'))

model.compile(loss='categorical_crossentropy',

optimizer='rmsprop',

metrics=['acc'])

history = model.fit(train_data, labels_train,

batch_size=64,

epochs=8,

validation_data=(test_data, labels_test))

Train on 50104 samples, validate on 16702 samples

Epoch 1/8

50104/50104 [==============================] - 1310s 26ms/step - loss: 0.7421 - acc: 0.7711 - val_loss: 0.5399 - val_acc: 0.8337

Epoch 2/8

50104/50104 [==============================] - 1277s 25ms/step - loss: 0.4833 - acc: 0.8511 - val_loss: 0.4706 - val_acc: 0.8546

Epoch 3/8

50104/50104 [==============================] - 1257s 25ms/step - loss: 0.4076 - acc: 0.8736 - val_loss: 0.4423 - val_acc: 0.8619

Epoch 4/8

50104/50104 [==============================] - 1254s 25ms/step - loss: 0.3588 - acc: 0.8882 - val_loss: 0.4365 - val_acc: 0.8641

Epoch 5/8

50104/50104 [==============================] - 1253s 25ms/step - loss: 0.3195 - acc: 0.9003 - val_loss: 0.4372 - val_acc: 0.8627

Epoch 6/8

50104/50104 [==============================] - 1254s 25ms/step - loss: 0.2844 - acc: 0.9121 - val_loss: 0.4436 - val_acc: 0.8668

Epoch 7/8

50104/50104 [==============================] - 1255s 25ms/step - loss: 0.2528 - acc: 0.9211 - val_loss: 0.4605 - val_acc: 0.8638

Epoch 8/8

50104/50104 [==============================] - 1253s 25ms/step - loss: 0.2241 - acc: 0.9293 - val_loss: 0.4652 - val_acc: 0.8660

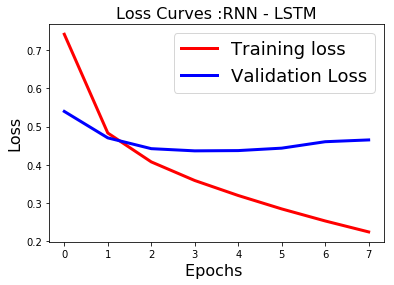

fig1 = plt.figure()

plt.plot(history.history['loss'],'r',linewidth=3.0)

plt.plot(history.history['val_loss'],'b',linewidth=3.0)

plt.legend(['Training loss', 'Validation Loss'],fontsize=18)

plt.xlabel('Epochs ',fontsize=16)

plt.ylabel('Loss',fontsize=16)

plt.title('Loss Curves :RNN - LSTM',fontsize=16)

plt.show()

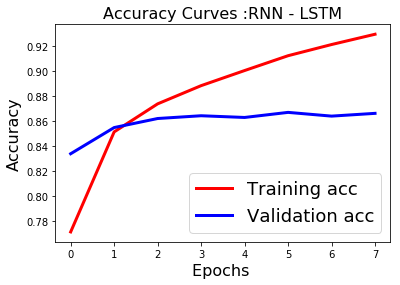

fig1 = plt.figure()

plt.plot(history.history['acc'],'r',linewidth=3.0)

plt.plot(history.history['val_acc'],'b',linewidth=3.0)

plt.legend(['Training acc', 'Validation acc'],fontsize=18)

plt.xlabel('Epochs ',fontsize=16)

plt.ylabel('Accuracy',fontsize=16)

plt.title('Accuracy Curves :RNN - LSTM',fontsize=16)

plt.show()

#predictions on test data

predicted=model.predict(test_data)

predicted

array([[2.9473981e-02, 5.8993626e-02, 4.3549597e-02, ..., 5.3076059e-05,

1.3519236e-04, 1.2607176e-03],

[3.1708100e-06, 1.8824825e-06, 8.0941909e-06, ..., 7.0293162e-08,

2.5478477e-07, 2.2799176e-07],

[5.1917366e-05, 3.2579785e-03, 3.9557324e-04, ..., 8.9214521e-04,

1.2622815e-05, 1.0268978e-04],

...,

[6.2825915e-04, 2.6230406e-04, 2.4657818e-03, ..., 3.9619839e-04,

1.0792948e-04, 2.8784707e-04],

[8.9328067e-04, 7.0826914e-05, 1.2235477e-05, ..., 1.4756889e-05,

5.9403064e-06, 1.5696751e-05],

[2.0625525e-06, 1.6432181e-05, 7.9930272e-05, ..., 5.1964469e-07,

4.3840672e-07, 5.2408077e-06]], dtype=float32)

#model evaluation

import sklearn

from sklearn.metrics import precision_recall_fscore_support as score

precision, recall, fscore, support = score(labels_test, predicted.round())

print('precision: \n{}'.format(precision))

print('recall: \n{}'.format(recall))

print('fscore: \n{}'.format(fscore))

print('support: \n{}'.format(support))

print("############################")

precision:

[0.88605578 0.76874206 0.86121571 0.9061445 0.86812444 0.71794872

0.93198339 0. 0.55333333 0.76068376 0.91164659]

recall:

[0.77871148 0.6576087 0.80776993 0.85696041 0.87762078 0.6746988

0.96246649 0. 0.45604396 0.82790698 0.85338346]

fscore:

[0.82892285 0.70884593 0.83363707 0.88086643 0.87284678 0.69565217

0.94697969 0. 0.5 0.79287305 0.8815534 ]

support:

[1428 920 1982 3132 4388 166 3730 27 182 215 532]

############################

print(classification_report(labels_test, predicted.round(),target_names=df1['product'].unique()))

precision recall f1-score support

Debt collection 0.89 0.78 0.83 1428

Consumer Loan 0.77 0.66 0.71 920

Mortgage 0.86 0.81 0.83 1982

Credit card 0.91 0.86 0.88 3132

Credit reporting 0.87 0.88 0.87 4388

Student loan 0.72 0.67 0.70 166

Bank account or service 0.93 0.96 0.95 3730

Payday loan 0.00 0.00 0.00 27

Money transfers 0.55 0.46 0.50 182

Other financial service 0.76 0.83 0.79 215

Prepaid card 0.91 0.85 0.88 532

micro avg 0.88 0.85 0.87 16702

macro avg 0.74 0.70 0.72 16702

weighted avg 0.88 0.85 0.87 16702

samples avg 0.85 0.85 0.85 16702

After hours of training we get good results with LSTM(type of recurrent neural network) compared to CNN. From the learning curves it is clear the model needs to be tuned for overfitting by selecting hyperparameters such as no of epochs via early stopping and dropout for regularization.

We could further improve our final result by ensembling our xgboost and Neural network models by using Logistic Regression as our base model.